Payment fraud prevention is defined as the set of systems, controls, and practices that stop fraudulent financial transactions before they complete. Finance teams and business owners face mounting pressure to prevent payment fraud as attackers grow more sophisticated, targeting everything from accounts payable workflows to online payment portals. The most effective defense combines AI-driven transaction monitoring, internal controls like dual payment authority, and payee verification standards such as Confirmation of Payee (CoP). This guide covers each layer in concrete terms, so you can build a defense that stops fraud without blocking legitimate payments.

What are the most effective technology tools for preventing payment fraud?

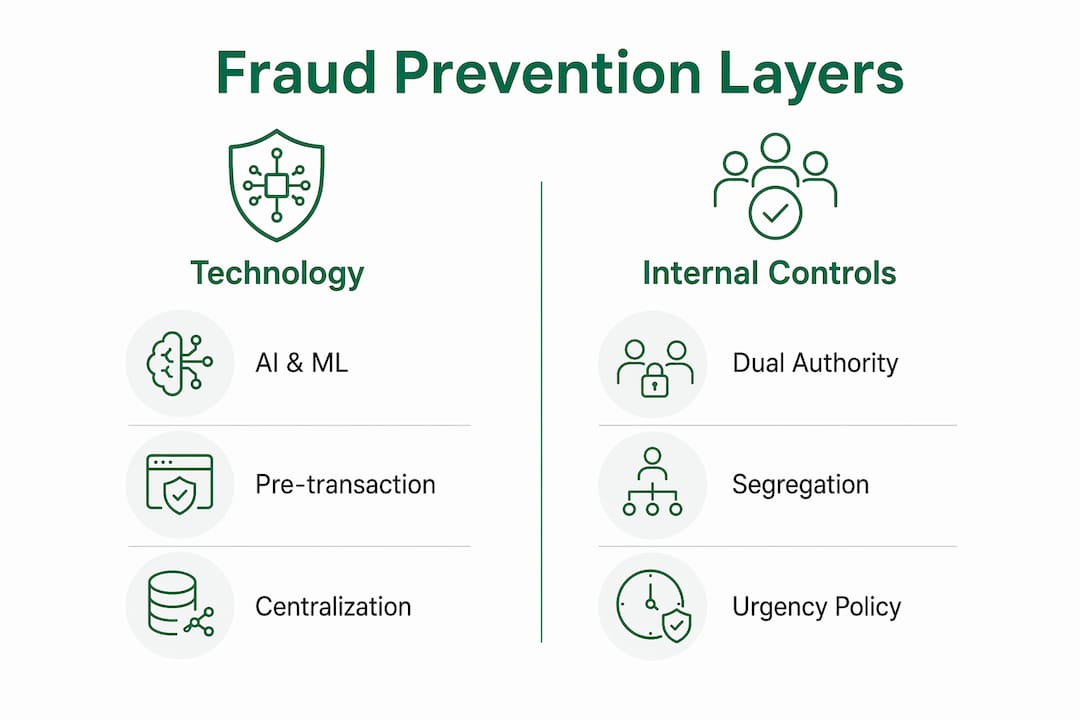

AI and machine learning are the strongest technology defenses available to finance teams today. These systems establish normal behavior baselines and flag transactions that deviate from expected patterns before payment is finalized. Unlike traditional rule-based systems, AI adapts to new fraud tactics without manual rule updates. That adaptability is what makes it superior for high-volume payment environments.

Pre-transaction controls form the next critical layer. Velocity limits, device fingerprinting, AVS/CVV verification, and 3D Secure authentication each block specific attack vectors before a transaction clears. Setting granular thresholds on these controls blocks high-risk transactions while keeping friction low for legitimate customers. Finance teams that configure these controls at the payment gateway level gain protection without adding manual review steps.

Centralizing payment operations through a payment hub enforces consistent security policies across every platform the business uses. Without centralization, security gaps appear wherever payment channels operate under different rules. A payment hub closes those gaps by applying the same controls to every outgoing transaction, regardless of channel.

| Technology tier | Key features | Primary benefit |

|---|---|---|

| Basic | Rule-based filters, velocity limits | Blocks known fraud patterns quickly |

| Intermediate | Device fingerprinting, AVS/CVV, 3D Secure | Reduces card-not-present fraud |

| Advanced | AI/ML anomaly detection, behavioral analytics | Catches novel fraud in real time |

Pro Tip: Apply tiered friction based on risk score. Low-risk transactions clear automatically. High-risk transactions trigger out-of-band verification. This approach preserves conversion rates while maintaining security where it matters most.

Which internal controls best reduce payment fraud risk?

Dual payment authority is the single most effective internal control for stopping fraudulent outgoing payments. Requiring two separate approvals for any payment instruction means a single compromised employee or email account cannot authorize a transfer alone. This control is especially critical for high-value or urgent payments, which fraudsters deliberately target because urgency suppresses scrutiny.

Segregation of duties separates the employee who approves vendor data from the employee who processes payments. When one person controls both functions, fraud becomes far easier to commit and conceal. Documented approval workflows make this separation enforceable and auditable.

Employee training on phishing, social engineering, and unusual payment requests builds the human layer of defense. Technology alone cannot stop an employee who has been manipulated into authorizing a fraudulent transfer. Training creates a team that recognizes manipulation tactics before acting on them.

A strong internal control program follows these steps:

- Document every payment approval workflow in writing, including who approves what and at which dollar threshold.

- Separate vendor master data management from payment processing across different roles.

- Require dual authorization for all payments above a defined threshold, with no exceptions for urgency.

- Train all finance staff quarterly on current phishing and social engineering tactics.

- Conduct monthly audits of user access rights to payment systems to remove stale permissions.

- Log every change to vendor payment details and require manager sign-off before the change takes effect.

Pro Tip: Manufactured urgency is a core fraudster tactic. Build a written policy that any payment request marked "urgent" by email automatically triggers a phone verification call to a pre-stored contact. Urgency should slow your process down, not speed it up.

How can businesses verify payee information to avoid payment diversion?

Independent verification is the most reliable method to confirm any change in payment details. Calling a pre-verified vendor contact using a phone number stored in your own records, not one provided in the email requesting the change, stops invoice redirection fraud before it succeeds. Failures to verify independently have caused significant financial losses across industries.

Account validation services match payee names against IBANs or bank account numbers before payment is sent. Confirmation of Payee (CoP) is the regulatory standard for this in the UK, requiring banks and payment service providers to check that the account name matches the account number provided. Vopify's UK Confirmation of Payee service delivers this check in under two seconds, covering both individual and business accounts.

For businesses operating across Europe, SEPA-compliant payee verification matches names against IBANs across 20 Eurozone countries. Vopify has processed over 10,000 verifications on this network, giving finance teams a reliable check before any cross-border payment clears. For high-volume accounts payable operations, bulk IBAN verification handles thousands of payees by CSV upload, removing the bottleneck of manual checks.

Best practices for payee verification:

- Store all vendor contact details in a system of record that is separate from email communications.

- Never use contact information provided in a payment change request to verify that same request.

- Run account validation on every new vendor before the first payment is made.

- Re-verify payee details after any reported change to banking information.

- Apply CoP or equivalent checks on all outgoing transfers, not just high-value ones.

What are the best practices for ongoing transaction monitoring?

Continuous monitoring catches fraud that pre-transaction controls miss. AI-driven monitoring watches for subtle deviations in transaction patterns, such as payments to new beneficiaries at unusual hours or amounts just below approval thresholds. These patterns are invisible to manual review at scale but detectable by machine learning models trained on your payment history.

Daily reconciliation of payment activity gives finance teams the earliest possible signal of a fraudulent transaction. Early identification is critical because the window to recall a payment closes quickly once funds leave the account. Teams that reconcile daily catch anomalies within 24 hours rather than at month-end.

Measuring the effectiveness of your fraud controls requires tracking multiple metrics simultaneously. Fraud rate, false-positive rate, and time-to-detect together give a complete picture of how well your defenses are working. Time-to-detect specifically measures how quickly your system identifies new fraud patterns, which reflects the health of your AI models.

| Monitoring strategy | Strength | Limitation |

|---|---|---|

| Rule-based alerts | Fast, predictable | Misses novel fraud patterns |

| AI anomaly detection | Adapts to new tactics | Requires training data and tuning |

| Daily reconciliation | Catches post-auth fraud early | Depends on staff discipline |

| Manual review queues | Human judgment on edge cases | Creates bottlenecks at volume |

What common mistakes create payment fraud vulnerabilities?

Over-reliance on manual processes is the most common vulnerability in mid-sized finance teams. Manual reviews cannot scale with transaction volume, and they introduce inconsistency. Fraudsters exploit that inconsistency by timing attacks during high-volume periods when staff are most likely to approve without full scrutiny.

Treating all friction points equally is a costly mistake. Applying friction selectively based on risk score preserves the experience for legitimate transactions while concentrating verification effort where it matters. Applying the same level of scrutiny to every transaction wastes resources and frustrates legitimate customers.

Common pitfalls and how to correct them:

- Pitfall: Verifying payment changes using contact details from the change request email. Fix: Always call a pre-stored, independently sourced contact number.

- Pitfall: Treating fraud rate as the only success metric. Fix: Track false-positive rate and time-to-detect alongside fraud rate.

- Pitfall: Skipping payee verification for existing vendors. Fix: Re-verify all vendors annually and after any reported banking change.

- Pitfall: Relying on static rule sets without regular updates. Fix: Review and update detection rules quarterly, and supplement with AI monitoring.

- Pitfall: Siloing fraud prevention in the IT department. Fix: Make fraud awareness a finance team responsibility with regular cross-functional training.

Key Takeaways

Preventing payment fraud requires layered controls: AI monitoring, dual authorization, and verified payee identity working together, not in isolation.

| Point | Details |

|---|---|

| Layer your defenses | Combine AI detection, pre-transaction controls, and internal approvals for full coverage. |

| Verify payees independently | Always confirm payment detail changes by calling a pre-stored contact, never the number in the email. |

| Train staff on urgency tactics | Manufactured urgency is a primary fraud vector; a pause-and-verify policy neutralizes it. |

| Monitor the right metrics | Track fraud rate, false-positive rate, and time-to-detect together for a complete picture. |

| Automate payee validation | Use account validation services like Vopify to match names against IBANs before every transfer. |

What I've learned about building a fraud-resistant payment culture

Technology solves the scale problem. Culture solves the human problem. After working with finance teams across industries, the pattern I see most often is organizations that invest heavily in detection software but leave their approval workflows unchanged. The software flags the anomaly. The employee overrides the flag because a senior manager sent the email. The fraud succeeds.

The fix is not more technology. The fix is a written policy that explicitly states: no payment instruction received by email alone, regardless of sender, bypasses verification. That policy has to come from leadership and be enforced without exceptions. When an employee sees a CFO-impersonation email and feels safe enough to pause and call the real CFO, the culture is working.

The second lesson I keep returning to is that internal culture is as important as any technical control. Employees must feel safe questioning unusual payment requests, even when the request appears to come from someone senior. Organizations that punish employees for slowing down a fraudulent payment are training their teams to approve the next one.

Fraud tactics evolve faster than most rule sets. The teams that stay ahead are the ones that treat fraud prevention as a continuous process, not a one-time implementation. Review your controls quarterly. Test your staff with simulated phishing exercises. Measure time-to-detect and act on it when the number rises.

— David

How Vopify fits into your fraud prevention strategy

Payee verification is the gap that most fraud prevention stacks leave open. Technology can monitor transactions and flag anomalies, but if the payment goes to the wrong account because the IBAN was never validated against the account holder's name, the fraud has already succeeded.

Vopify closes that gap. The platform verifies payee names against IBANs instantly, covering 20 Eurozone countries and the UK, with results in under two seconds. Finance teams get SEPA-compliant verification and UK Confirmation of Payee in a single platform, with no lengthy contracts required. For accounts payable teams processing large vendor lists, bulk verification handles thousands of records by CSV upload. Whether you process ten payments a day or ten thousand, Vopify fits into your existing workflow and confirms that every payment reaches the intended account holder before funds leave your account.

FAQ

What is payment fraud prevention?

Payment fraud prevention is the set of controls, technologies, and policies that stop fraudulent transactions before they complete. Effective prevention combines AI monitoring, internal approval workflows, and payee identity verification.

How does Confirmation of Payee prevent misdirected payments?

Confirmation of Payee checks that the account name provided matches the actual account holder before a payment is sent. This stops both fraud and accidental misdirection caused by incorrect account details.

What is the most effective internal control for outgoing payments?

Dual payment authority, which requires two separate approvals for any payment instruction, is the most effective single control. It prevents a single compromised employee or email account from authorizing a fraudulent transfer.

How should finance teams respond to urgent payment requests by email?

Any payment request marked urgent by email should trigger an immediate phone call to a pre-stored vendor contact. Manufactured urgency is a primary tactic used to bypass normal verification steps.

Which metrics best measure fraud prevention effectiveness?

Tracking fraud rate, false-positive rate, and time-to-detect together gives the most complete view. Focusing on fraud rate alone misses the business cost of blocking legitimate transactions.