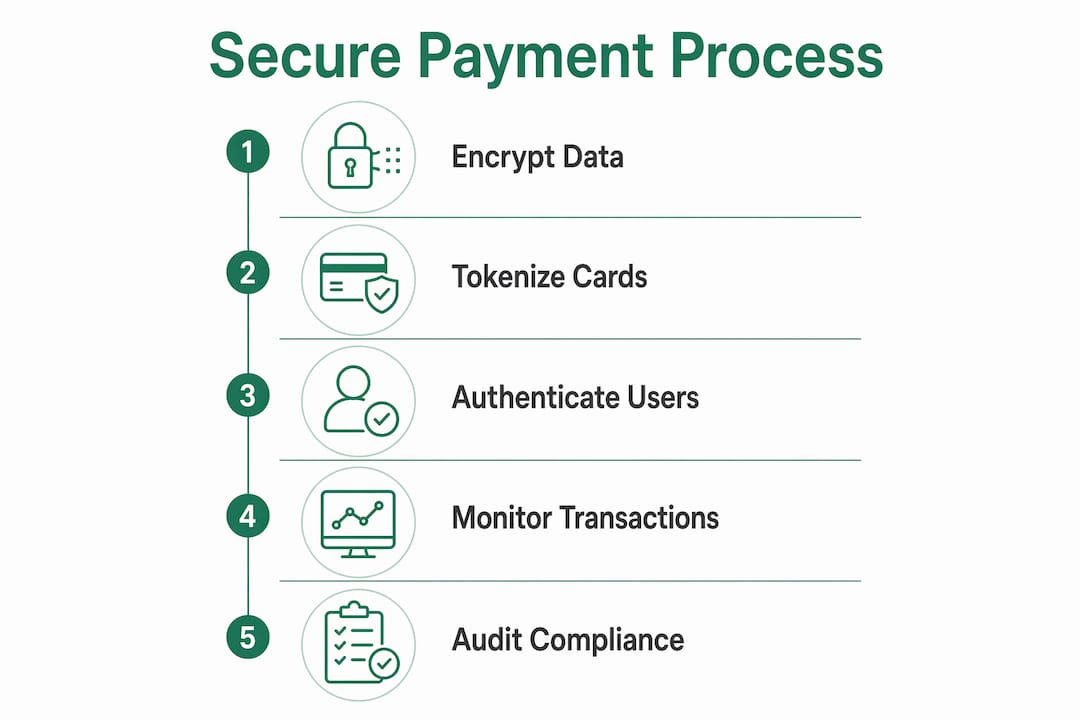

A secure payment process is defined as the end-to-end protection of financial data and transactions, from the moment a customer enters payment details through to final settlement. For finance professionals and business owners, this means combining tokenization, encryption, strong authentication, and real-time monitoring into a single, auditable framework. Standards like PCI DSS 4.0 and EMV 3-D Secure 2.3.1 set the baseline requirements, and global fraud losses are projected to reach $362 billion by 2028. That figure makes one point clear: payment security is not optional infrastructure. It is a core business function.

The industry term for this discipline is payment security, and the phrase "secure payment process" describes how that security is applied operationally, step by step, across every transaction your business handles.

What are the essential components of a secure payment process?

A payment gateway is the control center of any secure checkout solution. It handles fraud filtering, enforces tokenization, and generates the detailed logs that compliance audits require. Treating the gateway as a passive relay is the most common structural mistake finance teams make. Payment gateways should actively enforce security rules, not just route transactions.

Tokenization: network tokens vs. vault tokens

Tokenization replaces raw card numbers (PANs) with non-sensitive substitutes called tokens. Two types matter here. Network tokens are issued directly by card networks like Visa and Mastercard and travel with the card across devices. Vault tokens are generated internally and stored in a token vault backed by hardware security modules (HSMs), which isolate sensitive card data from your internal systems. Businesses using network tokenization see 30% lower fraud rates and 3–4% higher payment approval rates compared to those using standard PANs. That approval rate lift alone often justifies the implementation cost.

Encryption and authentication standards

Payment encryption techniques fall into two categories. Point-to-point encryption (P2PE) protects card data from the moment of capture at a terminal or browser field. Transport Layer Security (TLS) protects data moving between your servers and payment processors. Both are required. On the authentication side, EMV 3-D Secure 2.3.1 reduces false declines by sharing richer transaction context with card issuers, enabling better decisions without adding unnecessary friction for customers. Multi-factor authentication (MFA), aligned with NIST 800-63-4, protects the administrative access points that surround your payment infrastructure.

Key tools that complete the picture:

- Hosted checkout pages: Redirect payment data handling to a trusted provider, reducing PCI scope and security complexity for your team.

- Fraud scoring engines: Assign risk scores to transactions in real time using device fingerprinting, velocity checks, and behavioral signals.

- API security controls: Rate limiting, signed requests, and IP allowlisting prevent unauthorized access to your payment endpoints.

How to implement each step of a secure payment process effectively

Building a secure payment process from scratch, or upgrading an existing one, follows a clear sequence. Skipping steps creates gaps that attackers find faster than auditors do.

-

Capture card data in isolation. Use hosted payment fields, iframes, or mobile SDKs that collect card data directly into the payment provider's environment. Your servers never touch raw card numbers. This single step eliminates the most common source of PCI scope expansion.

-

Encrypt data at every layer. Apply TLS 1.3 between the browser and your backend. Confirm your processor uses P2PE from the point of capture. Encryption in transit and at rest are separate requirements. Both must be active simultaneously.

-

Tokenize immediately after capture. The moment card data reaches the payment provider, it should be replaced with a token. Tokenization reduces PCI audit scope significantly, but it does not eliminate PCI compliance entirely. You still need to manage token lifecycle, including expiration and re-issuance when cards are replaced.

-

Configure your gateway's fraud rules. Set velocity limits (maximum transactions per card per hour), block high-risk geographies where your business does not operate, and enable 3D Secure for transactions above your defined risk threshold. Review these rules quarterly, not annually.

-

Deploy risk-based authentication. EMV 3-D Secure 2.3.1 allows issuers to approve low-risk transactions without a challenge step. Risk-based authentication challenges customers only when signals indicate elevated risk, which preserves conversion rates while maintaining security. Blanket challenges on every transaction increase cart abandonment without meaningfully reducing fraud.

-

Enable real-time controls on instant payment rails. FedNow and RTP transactions settle in seconds, which leaves no window for manual review. Real-time velocity limits and first-payee cooldowns are the primary defenses against Authorized Push-Payment (APP) scams on these networks.

Pro Tip: Set a daily transfer cap on new payees for the first 72 hours after they are added to your system. This single control stops the majority of APP fraud attempts before they complete.

What are the most common pitfalls in securing payment transactions?

Finance teams that implement security controls often underestimate how quickly gaps appear in practice. These are the failure points that cause the most damage.

-

Treating tokenization as complete security. Tokenization reduces risk and audit scope, but it does not protect against account takeover, social engineering, or insider threats. It is one layer, not the whole defense.

-

Inconsistent token use across channels. A business might tokenize card data in its web checkout but store raw PANs in a legacy mobile app or call center system. That inconsistency expands PCI scope and creates an unmonitored attack surface.

-

Neglecting token lifecycle management. Tokens tied to expired or replaced cards cause payment failures. A card replacement program that does not automatically update network tokens creates both a security gap and a revenue loss.

-

Setting MFA too strict or too loose. Overly aggressive MFA on low-risk transactions drives customers away. Insufficient MFA on high-value or administrative transactions invites fraud. PCI DSS 4.0 requires MFA for all access to the cardholder data environment, with no exceptions.

-

Ignoring instant payment fraud. Push-payment scams on FedNow and RTP are growing faster than fraud controls on those networks. First-payee cooldowns and daily caps are not optional features. They are essential countermeasures.

"Transaction monitoring before, during, and after authorization is the only way to detect fraud patterns that no single rule catches. Businesses that monitor only at authorization miss account takeover, refund abuse, and velocity attacks that unfold across multiple sessions."

Comprehensive transaction monitoring catches fraud patterns that point-in-time controls miss entirely. Build monitoring into every stage of the transaction lifecycle, not just the authorization moment.

How to maintain and audit your payment security for ongoing compliance

Payment security degrades without active maintenance. Standards evolve, attackers adapt, and internal processes drift. A structured maintenance program prevents all three.

PCI DSS 4.0 compliance requires finance teams to focus on four areas: MFA coverage across all cardholder data environment access points, enhanced logging with tamper-evident audit trails, accurate inventory of all systems that store or transmit card data, and customized implementation approaches for controls that do not fit standard templates.

Pro Tip: Run a quarterly token inventory audit. Identify every system that holds a token or a PAN, map it to a business function, and decommission any that no longer serve an active purpose. Orphaned tokens are a compliance liability.

ISO 20022 payment messages carry richer transaction context than legacy formats, including purpose codes, legal entity identifiers, and structured remittance data. Finance teams that use this data for transaction screening catch more fraud with fewer false positives than those relying on legacy message formats alone.

| Maintenance activity | Recommended frequency |

|---|---|

| PCI DSS internal review (MFA, logs, inventory) | Quarterly |

| Fraud rule review and velocity limit adjustment | Quarterly |

| Platform and API patch cycle | Monthly or per vendor advisory |

| Employee fraud awareness training | Annually, with incident-triggered refreshers |

| Penetration testing of payment endpoints | Annually (PCI DSS 4.0 requirement) |

| Token inventory and lifecycle audit | Quarterly |

Staying current with regulatory updates is not optional. The Reserve Bank of India's payment security directions, FedNow operating rules, and GDPR/PIPL data handling requirements all affect how you store, process, and transmit payment data. Assign a named owner to track regulatory changes and translate them into system updates within 90 days of publication.

Key Takeaways

A secure payment process requires tokenization, encryption, risk-based authentication, and continuous transaction monitoring working together, with PCI DSS 4.0 compliance as the non-negotiable baseline.

| Point | Details |

|---|---|

| Tokenize immediately | Replace PANs with tokens at capture to reduce PCI scope and cut fraud rates by up to 30%. |

| Use risk-based authentication | EMV 3-D Secure 2.3.1 challenges only high-risk transactions, protecting conversion rates without sacrificing security. |

| Treat your gateway as a security hub | Configure fraud rules, velocity limits, and logging actively. A passive gateway is a liability. |

| Monitor every transaction stage | Fraud detection before, during, and after authorization catches patterns that authorization-only controls miss. |

| Audit on a fixed schedule | Quarterly reviews of MFA, token inventory, and fraud rules prevent compliance drift and close emerging gaps. |

Why I think most businesses get payment security backwards

Finance teams tend to implement payment security as a compliance project. They work toward a PCI audit, check the required boxes, and then treat the work as done until the next audit cycle. That approach is exactly wrong.

The businesses I have seen handle payment security well treat it as an operational discipline, not a certification exercise. They review fraud rules every quarter because attack patterns shift every quarter. They test their authentication flows against real abandonment data because a 3-D Secure challenge that adds four seconds to checkout costs real revenue. Security that drives customers away is not good security. It is a different kind of loss.

The network tokenization data makes this concrete. A 3–4% lift in payment approvals from network tokens is not a security metric. It is a revenue metric. The best payment security implementations I have encountered are the ones where the security team and the revenue team are reading the same dashboard.

The other thing most articles get wrong: payee verification is treated as an afterthought. Encrypting the card data in transit means nothing if the payment lands in the wrong account because no one verified the IBAN against the account holder's name. That is where a significant share of business payment fraud actually happens, and it is the gap that most secure checkout solutions do not address.

— David

How Vopify strengthens your payment verification layer

Encryption and tokenization protect card data in transit. They do not verify that a bank transfer is going to the right person. Vopify fills that gap by confirming in real time that the IBAN you are paying matches the intended account holder's name, covering 20 Eurozone countries with a response time under two seconds.

For finance teams processing high volumes of outbound payments, bulk IBAN verification lets you validate thousands of payees by CSV before a single payment leaves your account. For SEPA transactions, Vopify's Verification of Payee service meets the EU's regulatory requirements directly. With over 10,000 verifications processed, Vopify gives accounts payable teams a fast, contract-free way to close the payee fraud gap that technical payment security alone cannot address. Start a verification at vopify.io.

FAQ

What is a secure payment process?

A secure payment process is the end-to-end protection of financial transactions, covering data capture, encryption, tokenization, authentication, and monitoring from initiation through settlement. PCI DSS 4.0 sets the current compliance baseline for businesses that handle card data.

How does tokenization improve online payment security?

Tokenization replaces raw card numbers with non-sensitive tokens, reducing PCI audit scope and cutting fraud rates. Businesses using network tokenization report 30% lower fraud rates and 3–4% higher approval rates compared to those using standard PANs.

What does PCI DSS 4.0 require that earlier versions did not?

PCI DSS 4.0 adds stronger MFA requirements for all cardholder data environment access, enhanced tamper-evident logging, and mandatory annual penetration testing of payment endpoints. It also introduces customized implementation options for controls that do not fit standard templates.

What is the biggest fraud risk on instant payment rails?

Authorized Push-Payment (APP) scams are the primary threat on FedNow and RTP networks, where transactions settle in seconds with no reversal window. First-payee cooldowns and daily transfer caps on new payees are the most effective countermeasures.

Does tokenization replace the need for payee verification?

No. Tokenization protects card data in transit but does not confirm that a bank transfer reaches the correct account holder. Payee verification services, such as those provided by Vopify, confirm that an IBAN matches the intended recipient's name before the payment is sent.